S&P 500 Companies’ Disclosed Political Spending

by Type of Recipient

by Type of Recipient

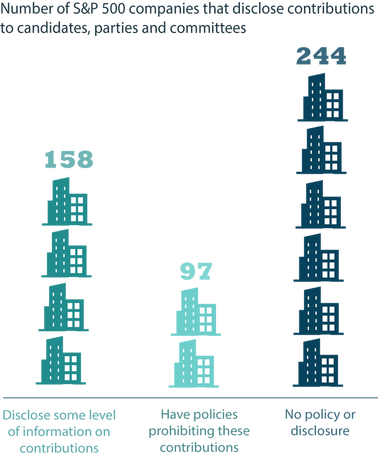

Corporations are prohibited from tapping corporate treasuries for direct contributions to federal candidates and national political parties.

However, in many states they may donate directly to state and local candidates, parties, and committees within certain limits (see here).

State-level candidate, party, and committee contributions must be disclosed to varying degrees and can be found on state campaign finance databases.

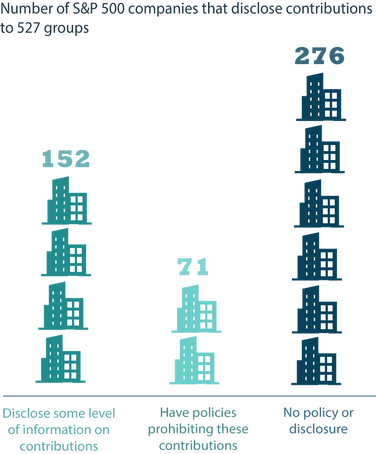

Corporations may also give to tax-exempt political committees organized under § 527 of the Internal Revenue Code, or 527 groups. These groups are devoted to election-related activity and may engage in independent spending, but must disclose their donors to the IRS.

The Center for Responsive Politics maintains a list of the top fifty 527 groups by election cycle (see here).

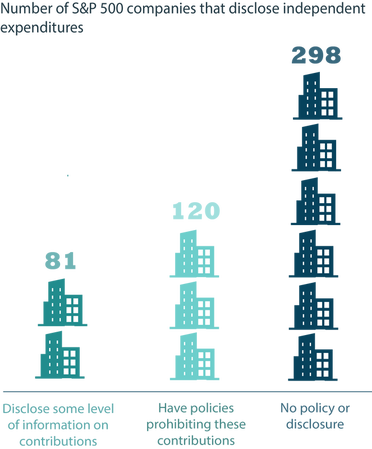

Corporations may use treasury funds for direct independent expenditures. This allows them to fund advertising that targets or promotes a specific candidate so long as the effort is undertaken independently from the candidate’s campaign or party committee.

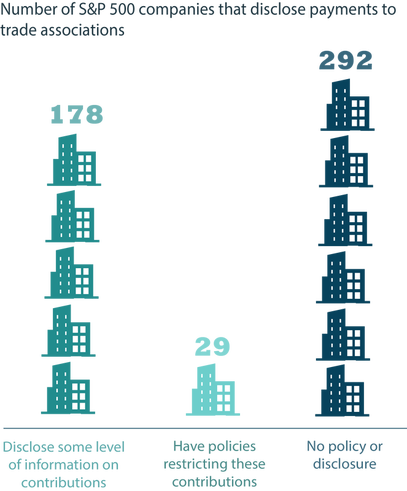

Companies may give unlimited sums to trade associations organized under § 501(c)(6) of the Internal Revenue Code. These tax-exempt groups must have a “primary purpose” other than influencing elections, but they are permitted to engage in election-related activity.

Unlike many political committees regulated by federal election law, trade associations are not required to disclose their donors. However, corporate funds that are used by trade associations for election-related activity are non-deductible for tax purposes.

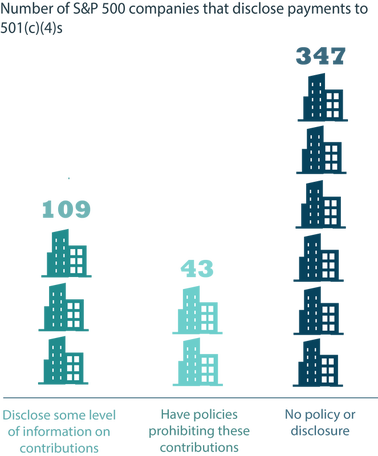

Groups organized under § 501(c)(4) of the Internal Revenue Code, sometimes called “social welfare” organizations, may also keep their donors secret. These groups may use their funds for election-related activity so long as it is not their primary purpose.

Ballot measures – also known as ballot initiatives, questions, or propositions – are pieces of proposed legislation to be approved or rejected directly by voters. Corporations may spend unlimited sums to support or oppose ballot measures.

What does

your company

spend?

How does

your company

rank?

Do you

have our

new report?

What does

your company

spend?

How does

your company

rank?

Do you

have our

new report?